")

As Generative AI impacts drug research, this thesis aims to uncover the opportunities for Exscientia plc (NASDAQ:EXAI) and show it is a buy based on the strength of its technology platform. Noteworthily, I was again bullish when covering the stock in April 2022 priced at $12. It did rise to $15.21, but, subsequently, slid to $4.28 as the Federal Reserve hiked interest rates at such an aggressive pace only seen in the Paul Volcker Era.

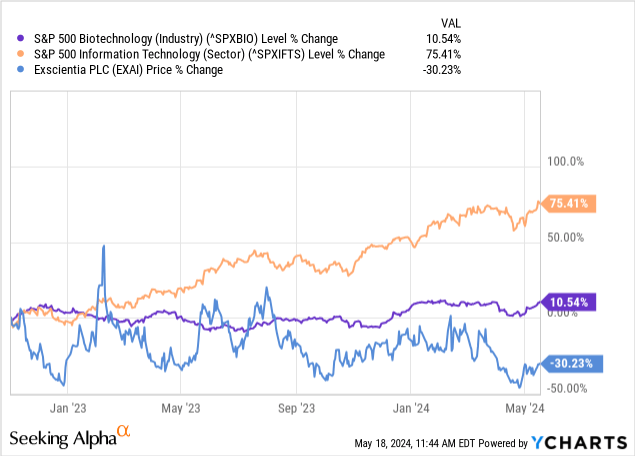

Trading at around $5 at the time of writing, the stock has underperformed the S&P 500 Biotech and S&P 500 IT sectors as shown below, something abnormal considering the cash position, potential path to profitability, and artificial intelligence opportunities.

First, research by BCG (Boston Consulting Group) illustrates how AI is concretely making a difference in pharmaceutical R&D.

How AI is Disrupting Pharmaceutical R&D

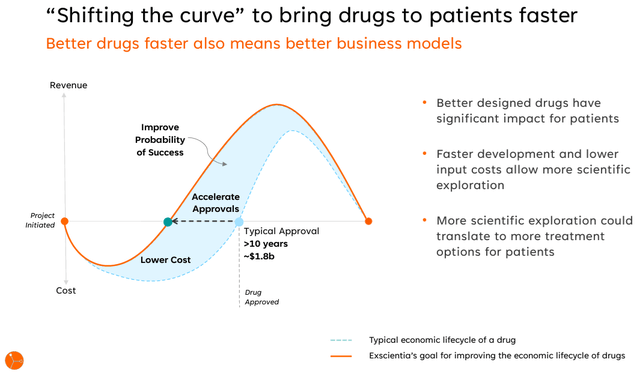

Traditional procedures in drug research take time and cost a lot of money since they involve five steps, including clinical trials. Even before clinical research where the potential drug candidate is tested on human beings, it must be identified in the lab and undergo preclinical testing on animals. After clinical developments, the new drug is submitted to the health authorities for approval and marketing. Then begins a long period of monitoring for its side effects, all taking 10 years or more.

This encourages the adoption of artificial intelligence to accelerate approvals and reduce time to market, just like Exscientia is doing. Already present in the space for more than a decade, it is innovating with its new automation facility for integrating AI design with automated experimentation, which can potentially reduce drug development and deployment time from a decade to a “handful of years” suggesting a faster return on investment.

Company presentation (Exscientia IR)

Looking across the industry, according to researchers from BCG, AI-derived molecules have shown higher success than the average rate of 80%–90% for phase I of clinical development, explained by the rapid scanning of vast data sets to screen key details like toxicity effects. Thus, using intelligent software accelerates drug development time while improving the quality.

How Exscientia Differentiates Itself from Big Data Companies and Other Biotech Using Gen AI

However, when it comes to applying technology to biotech research, this is not a novel idea and has been around for years and well before the advent of ChatGPT as exemplified by the collaboration between big data companies like International Business Machines (IBM) in the context of the High Performance Computing Consortium for accelerated development of the COVID-19 vaccine. At present, giant cloud service providers like Alphabet (GOOG) have invested billions of dollars to build intelligent infrastructures that big pharma can tap into instead of partnering with Exscientia.

Thus, for Exscientia, product differentiation is key, and, it focuses on specifics like identifying the molecule that can be used for delivering a cure for a particular disease through its tech platform built using data from twelve years of experience designing drugs using technology.

Looking specifically into Gen AI, by May 2023 Exscientia had already created the sixth molecule to enter the clinical stage through its Generative AI platform. By comparison, Recursion Pharmaceuticals (RXRX) announced a collaboration with NVIDIA (NVDA) in July last year to accelerate the training of its AI models on the semiconductor giant’s DGX cloud. This would eventually be released on BioNeMo, Nvidia’s cloud service for Generative AI in drug discovery.

Company presentation (Exscientia IR)

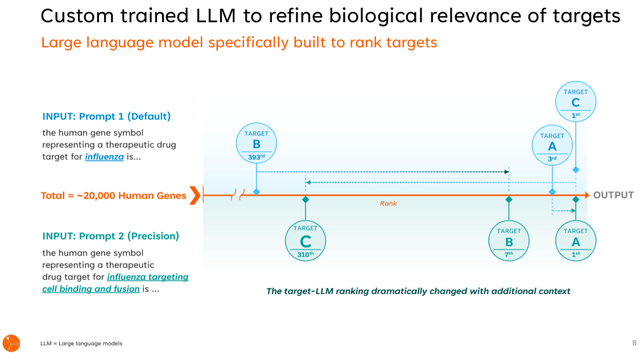

Therefore, this remains a competitive space, and Recursion benefits from Nvidia’s computational power together with eleven years of data to feed its LLMs, (large language models). However, Exscientia currently seems to be ahead in designing Gen AI-based molecules. The reason is that it has integrated the software that manages the synthesis of molecules and the experimentation feature in the Generative AI design itself. In this way, the computational environment is close to the actual lab setup.

In this context, Gen AI models can provide a proactive idea of the drug target interactions for example when trying to identify an antiviral cure without actually having to do the testing physically, making it possible to rapidly select the best compound during a study.

Finances and Risks

However, even after reducing the development time for new drugs, the company has to spend money building its platform with $33.7 million spent last year alone.

In this respect, while it is well capitalized with $463 million in cash versus $24 million of debt in FY-2023 which ended in December, it burnt $150 million in cash or more than double the amount in 2022. Also, its operating expenses of $213 million were at least nine times total revenues, showing that it may take time to break even.

This implies risks of contracting debt especially, when interest rates have skyrocketed, from 0.08% in early 2022 to 5.33%. It may also have to issue equity as in 2021 when $722 million worth of common stock was sold. However, at that time, each share was valued at over $20, or roughly four times the current value. Therefore, in the eventuality of an equity offering, it will have to issue more shares to obtain the same amount.

Therefore, the risk for investors is that it might have to finance growth through another potential share dilution in case of delay in monetizing its drug discovery programs. Furthermore, since it does not generate operational cash flow, this remains a rate-sensitive stock or one whose performance is determined by the hawkishness or dovishness of the Federal Reserve. Thus, despite my bullish thesis in April 2022 when it was trading at $12.13, it went all the way down to $4.28 as the Federal Reserve hiked interest rates at such an aggressive pace only seen in the Paul Volcker Era.

However, as per the management, the existing cash provides a runway well into 2026. I believe this is achievable based on the $463 million of cash held in the balance sheet at the end of 2023, and a total cash burn of $450 million assuming the yearly outflows continue at $150 million. However, this is a worst-case scenario that ignores partnership-led income.

Partnerships Generating Cash and the Path to Profitability

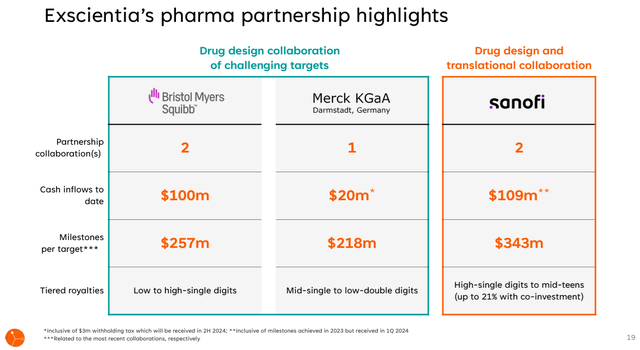

Thus, the biotech does not necessarily need to advance to stage 4 or the commercialization phase with clinical trials to monetize its pipeline. For this purpose, it has inked partnerships with major pharmaceutical companies like Sanofi (SNY), Bristol-Myers Squibb (BMY), and Merck KGaA (OTCPK:MKKGY) which have resulted in around $229 million of cash inflows to date for Exscientia as pictured below.

Company presentation (Exscientia IR)

Zeroing on the Sanofi strategic research collaboration, it was initiated in January 2022 to develop a pipeline for precision medicines using AI and focusing on oncology and immunology with an upfront cash payment of $100 million with $5.2 billion of potential milestones and royalty money. This agreement was expanded in December 2023 as part of a drug discovery stage program with Exscientia eligible to pocket up to $45 million of upfront fees and preclinical milestones payments in the first quarter of 2024.

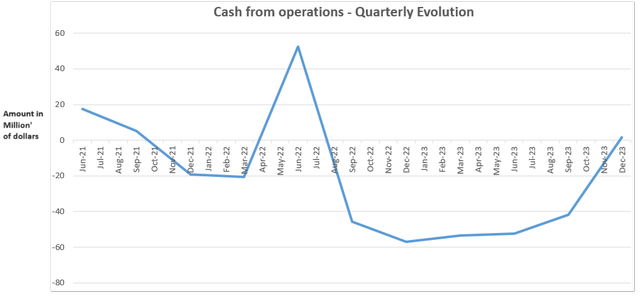

This means that cash burn may be less than last year and the chart below which shows the cash flow generated each quarter may sustain its uptrend.

Chart prepared using data from (Seeking Alpha)

Additionally, there is the possibility of obtaining over $300 million of sales-based royalties in the next 18 to 36 months from Sanofi while its Bristol Myers partnership has been expanded to include payments of $50 million up front with the possibility of obtaining $125 million in milestones, and tiered royalties.

This means an additional $425 million (300 + 125) to partially offset the roughly $212 million annual operating losses (based on 2022 and 2023) figures). The path to profitability becomes clearer when factoring firstly, efficiency-related gains where budgetary savings of around $60 million were made last year. Second, its differentiated platform can generate more sales as it remains active on the business development front this year.

A Buy Based on Tech Platform Strength

For this purpose, analysts’ consensus revenue estimate for FY-2024 is $73.5 million, or a YoY growth of 127% compared to a decline for FY-2023. Furthermore, for Sanofi to have expanded its agreement, this somehow validates Exscientia’s technological platform ability to have “solved a major limitation for a new class of drug” according to the CFO, Ben Taylor.

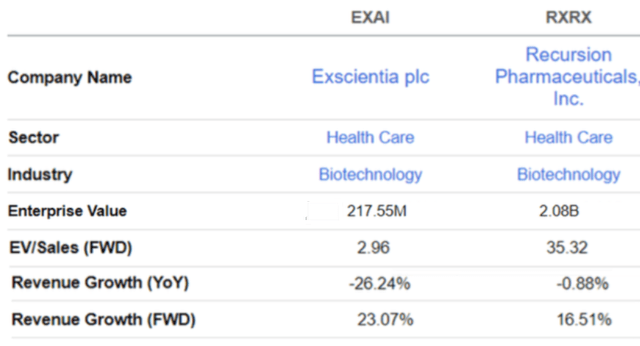

This means it deserves better, and for valuation purposes, I compare it with peer Recursion which has benefited from Nvidia acquiring a $50 million stake in its capital structure. However, it is Exscientia which is expected to generate higher growth on a forward basis as shown below, which means that it merits a better EV/Sales multiple than the 2.96x. Increasing by 50% results in a fairer multiple of around 4.5x, or roughly 8 times less than Recursion.

Comparison of metrics (Seeking Alpha)

Thus, incrementing the share price of $5 by 50%, I obtained a target of $7.5.

Now, the 50% figure may seem modest when comparing Wall Street’s average of $8.72, but remains a fair one because of the risks. For this matter, recent price action has been determined mainly by the higher probability of the Federal Reserve cutting interest rates sooner rather than later due to the lower-than-expected CPI print for April. At the same time, Moderna (MRNA) partnering with OpenAI to deploy chat-based interactive tools has created some synergy for the stock and others.

Another reason for my moderate target is that when I covered the stock last time, it was trading at a trailing P/S of around 17x compared to 25x now, or a 47% increase. Thus, in the absence of catalysts, expect volatility, but the stock remains well above its support level of $4 reached last month. Finally, considering its underperformance relative to tech and biotech as per the introductory chart, it remains reasonably priced given the attractiveness of its platform to big pharma.

Read the full article here

")

")

")