")

Things have gone well for Argentine equities since I last highlighted the election opportunity in Global X’s MSCI Argentina ETF (NYSEARCA:ARGT) (see ARGT: Positive Change Is Afoot For Argentina). In this post-election phase, though, all eyes are now on President Javier Milei’s ability to execute relative to expectations embedded in asset prices. On this front, a recent positive development was getting the all-important omnibus bill (also ‘Ley bases’) through the Argentine Senate. Yes, compromises were made, namely on certain taxes and privatization efforts. But early success here, particularly on reducing State bureaucracy, remains a positive signal for governance and bodes well ahead of mid-term elections next year – an opportunity for Milei and co to make further inroads into Congress.

Crucially for equities, new reforms pave the way for long-term shareholder value creation. Some of the deregulation efforts will admittedly take time to play out, but in the more immediate term, market-friendly schemes like RIGI (or the ‘Large Investments Incentive Regime’) should benefit the pipelines of Argentina’s biggest resources and energy players (key components of the ARGT portfolio). In the meantime, domestic demand will be an issue for earnings, though a recent slowing of sequential inflation numbers indicates an emerging path toward macro recovery. All in all, there are risks here, but given where valuations are and the low earnings base we are coming off, as well as the FX-hedged nature of large-cap balance sheets, ARGT continues to screen attractively as a call option on the future of Milei’s reforms.

ARGT Overview – The Premier Low-Cost Argentina Pure Play

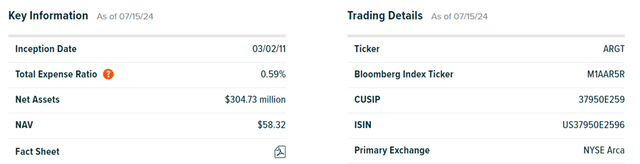

The Global X MSCI Argentina ETF remains the only US-listed tracker fund focused on the country. The index being tracked here, the MSCI All Argentina 25/50 Index, is also unchanged, as are its two key concentration limits – 1) no single holding over 25% of the index weight and 2) a cumulative cap of 50% on holdings with a >5% index weight. The biggest development, though, is that ARGT now manages a far larger ~$305m asset base. While the manager hasn’t passed this through to the expense ratio (still a relatively competitive ~0.6%), liquidity is much improved (~0.4% bid/ask spread), which bodes well for the overall cost (fees + execution).

Global X

ARGT Portfolio – Mind the Concentration

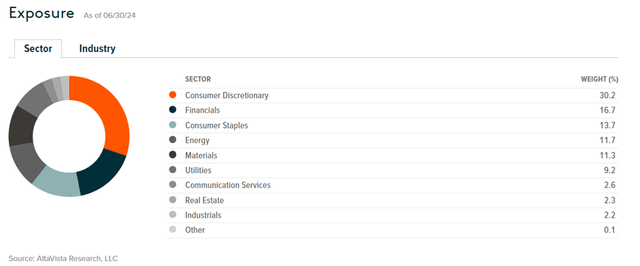

At 25 stocks (i.e., the minimum per MSCI policy), the fund has one less holding than when I last covered it. As a result, concentration levels are also slightly higher across the board. Sector-wise, Consumer Discretionary remains the largest exposure at 30.2%, with the industry breakdown suggesting that a lot of this comes from Retail (56.5%) and Hotels, Restaurants & Leisure (13.8%). Elsewhere, Financials is now the second largest at 16.7% after a very strong rally in recent quarters, while Materials (11.3%) and Utilities (9.2%) are smaller contributors. On a cumulative basis, the top five sectors account for an outsized ~84% of the total portfolio, so either way you slice it, ARGT is one of the most top-heavy single-country ETFs out there.

Global X

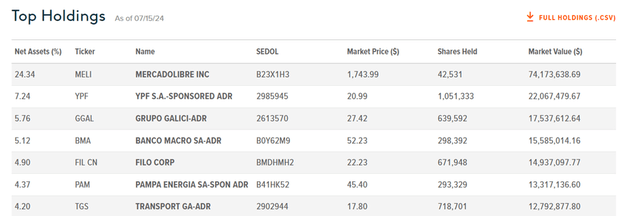

A glance at the ARGT single-stock breakdown shows that the increased % concentration applies here as well. The fund’s largest holding remains online marketplace MercadoLibre (MELI) at an upsized 24.3%, followed by state-owned energy company YPF SA (YPF) at 7.2%. Major financial services names like Grupo Financiero Galicia (GGAL) and Banco Macro (BMA) come next at 5.8% and 5.1%, respectively.

Global X

Besides the concentration, one other thing to note is that a lot of ARGT’s stock exposure is via foreign-listed depositary receipts and direct listings rather than local listings. While this can result in periodic premiums/discounts to the underlying, it does mitigate many of the difficulties associated with market access and FX, among others. In the meantime, ARGT’s portfolio is priced at ~13x earnings and ~1.6x book, though the outsized allocation to MELI (~50x earnings and ~18x book) distorts these metrics quite a bit; ex-MELI, equity valuations remain undemanding as a play on the broader reform story.

Global X

ARGT Performance – Post-Election Bounce Adds to an Impressive Track Record

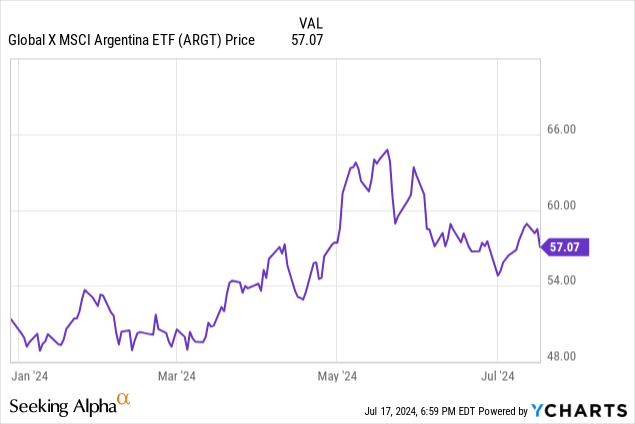

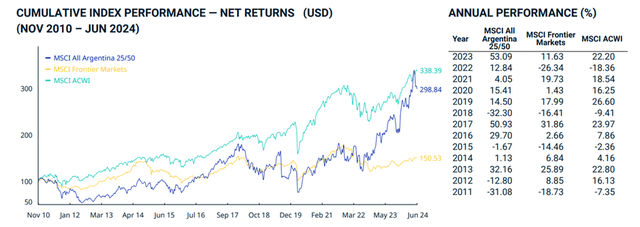

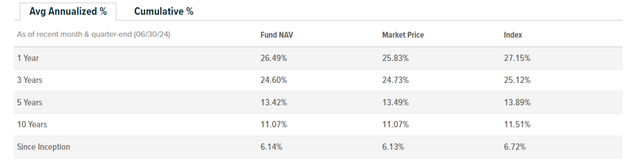

Argentine equities have built on their post-election momentum in H2 last year, as evidenced by ARGT appreciating by +11.3% year-to-date. Zooming out, this means the fund has now compounded by an annualized +6.1% since its inception in 2011 – just short of an equivalent MSCI global index tracker but well ahead of comparable frontier market index funds.

MSCI

Performance numbers get more impressive the shorter the timeline, with ARGT’s +11.1% annualized over the last decade more than matched by a +24.6% and +13.4% track record over the last three and five years, respectively. Also helping is the minimal tracking error after expenses – a result of the fund tracking an index of predominantly more accessible and liquid overseas listings.

Global X

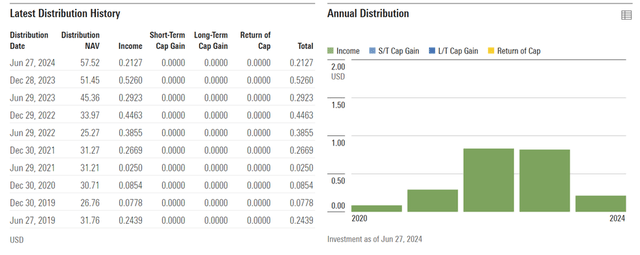

As for the semi-annual distribution, sourced entirely from the recurring income stream of ARGT’s cash-rich holdings, this year isn’t shaping up quite as well as last year. Recall that the June payout came in at $0.21/share – well below the $0.29/share previously on normalizing energy/commodities tailwinds. That said, the trailing yield on offer is still a very decent ~2%, and with the ARGT earnings base poised to benefit from structural reforms and an eventual macro normalization, there remains compelling income potential here.

Morningstar

A Call Option on Argentina’s Reform Story

Argentina’s reform progress, while not as abrupt as President Milei’s election promises, is moving in the right direction – the recent omnibus bill being a case in point. Further progress here bodes well for equities going forward, particularly with mid-term elections due next year and markets still a long way off pricing in a blue-sky reform or earnings reacceleration scenario. Net-net, ARGT’s reasonably valued portfolio remains an attractive call option on the structural reform story.

Read the full article here

")

")

")